Introduction

The European automotive industry stands at an inflection point where technological disruption is outpacing the current workforce's skills, creating an urgent need for strategic talent transformation [1, 2]. This critical juncture demands that traditional manufacturing excellence converge with cutting-edge technological innovation. This convergence defines what we term "automotive deep tech" – the integration of advanced artificial intelligence, sophisticated data analytics, revolutionary materials science, next-generation power electronics, seamless connectivity solutions, and autonomous systems into the core of automotive design, manufacturing, and operation [3, 4].

The scope of this analysis encompasses these specific deep tech domains as they intersect with automotive applications, distinguishing our focus from broader Industry 4.0 initiatives or general advanced manufacturing technologies. When we reference deep tech throughout this report, we are specifically addressing technologies that require significant R&D investment, possess high barriers to entry, and fundamentally alter traditional automotive value chains [3, 4].

The rapid acceleration of technological disruption – driven by electrification mandates [5, 6], autonomous vehicle development [10, 11], and connectivity requirements [7] – is creating a fundamental shift in talent needs that will reshape competitive advantage in the European automotive sector through 2030.

This transformation extends beyond simple digitalisation to encompass a complete reimagining of automotive engineering, manufacturing, and service delivery models. Our analysis incorporates the latest industry data through 2025, aligning with current consensus projections from leading automotive research institutions and regulatory frameworks [5, 6, 7, 8, 9, 12, 13].

The methodology underlying this report combines quantitative analysis of talent market data with qualitative insights from industry stakeholders across the European automotive ecosystem. We examine both established OEMs adapting to new technological paradigms and emerging mobility companies built on deep tech foundations. This dual perspective reveals not only what skills will be required, but how different organisational models will compete for increasingly scarce technical talent.

Methodological Note: Talent shortage projections and growth estimates throughout this report are based on analysis of multiple industry sources including IEA, ACEA, McKinsey, Eurofound and specialised automotive research firms. Percentage figures should be considered directional indicators rather than precise predictions, as methodologies vary across sources. Where specific statistics are cited, we have verified them against primary source material and noted limitations where appropriate. Industry scenario planning inherently involves uncertainty, and readers should validate projections against their specific organisational context [1, 2, 12, 14].

The strategic framework presented here addresses three critical questions: Which specific deep tech competencies will drive competitive advantage? How can automotive employers position themselves to attract and retain essential talent? What organisational capabilities will separate industry leaders from those left behind in this technological transition?

Executive Summary

The European automotive industry is undergoing a profound transformation driven by electrification, autonomous driving technologies, and changing consumer preferences [10, 11, 12, 13, 60]. This report examines the key trends shaping the industry between 2025 and 2030, with a focus on talent demands and how employers can position themselves for success in this rapidly evolving landscape.

Key Findings

- Technology Disruption: Electrification, autonomy, and software are transforming automotive; IEA 2025 expects the global EV share to exceed 40% by 2030, with Europe reaching 45-50% by 2030 under current realistic projections (revised from earlier 60% targets); data‑driven services are becoming core differentiators [12, 13].

- Talent Crisis: Severe shortages are projected in software, battery, and cyber roles; skills analysis shows critical gaps across Europe. The automotive ecosystem employs 6.72M workers in core subsectors (C29 + G45, Q3‑2024) [1] and ~14.6M across the wider ecosystem [16] — requiring strategic workforce development across all skill categories. Shortage estimates should be treated as directional given varying methodologies across sources [2, 15].

- Autonomous Reality Check: Level 2–3 will dominate through 2030; Level 4+ vehicles are unlikely to exceed ~5–6% of new sales before 2035 [10, 11].

- Deep Tech Integration: AI, advanced materials, power electronics, connectivity, and (select) quantum computing are becoming essential competencies, requiring hybrid hardware–software skill sets [4, 17, 69].

Key Strategic Actions

- Immediate Upskilling: Target 15–20% of the workforce for digital upskilling by 2026; launch reskilling pathways for mechanical engineers into electrical/software roles (align with the EU Digital Decade skills target) [2, 18].

- Strategic Hiring: Build pipelines now for battery, AI, and cybersecurity talent ahead of late‑decade demand peaks linked to EV penetration [12, 13, 15].

- HR Policy Reform: Offer flexible work and compensation aligned with tech‑sector benchmarks to attract software and data talent [2, 15].

- Partnership Strategy: Establish university collaborations (EV, software) and consider targeted acquisitions of deep‑tech startups to accelerate capability build‑up [16, 19].

Market Overview

The European automotive market continues to evolve rapidly as regulatory pressures, technological advancements, and shifting consumer preferences reshape the industry. With the EU's commitment to carbon neutrality by 2050 and interim targets for 2030, automotive manufacturers are accelerating their transition to electric vehicles while simultaneously investing in autonomous driving capabilities and connected car technologies.

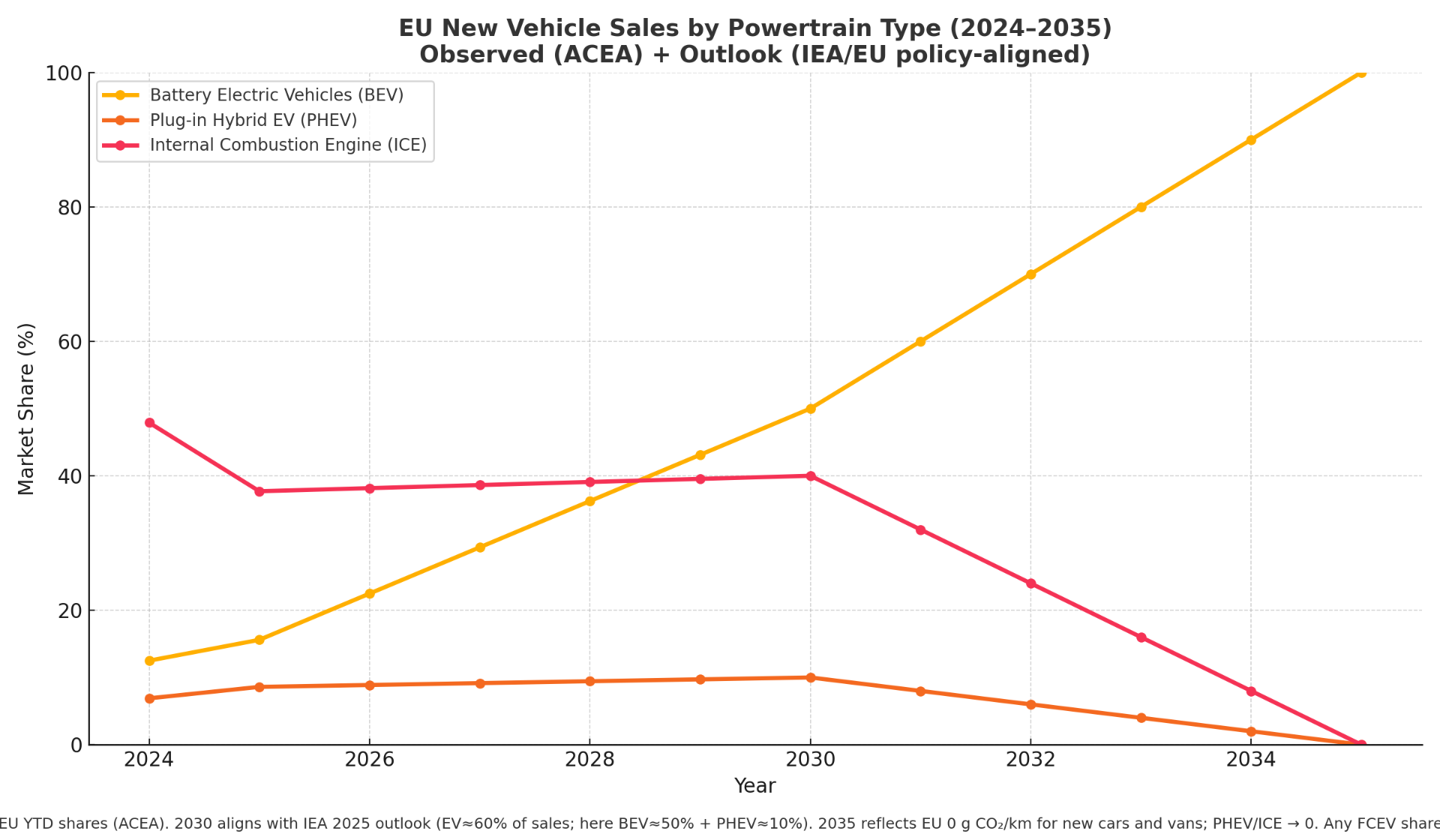

Revised EV Projections (2025): Industry consensus has shifted toward more realistic adoption timelines. Europe is now projected to reach 45-50% EV share by 2030, with the original 60% target delayed to 2035. This revision reflects infrastructure constraints, supply chain realities, and consumer adoption curves. The 60% European target remains achievable but requires additional policy support and infrastructure acceleration beyond current deployment rates. Revised Timeline

EU New Vehicle Sales by Powertrain Type

Chart Notes

Anchors used:

2024 YTD BEV 12.5%, PHEV 6.9%, ICE 47.9% (ACEA 2024 YTD baseline referenced by ACEA 2025 note); 2025 YTD BEV 15.6%, PHEV 8.6%, ICE 37.7% [29].

2030 reflects revised industry consensus: EV ≈45-50% (BEV ≈35-40% + PHEV ≈10%), ICE ≈45-50% — more conservative than earlier projections [30].

2035 reflects EU 0 g/km requirement: PHEV/ICE → 0; any small FCEV share is visualised within the BEV band to keep a three‑series view [31].

Method: linear interpolation between anchors for 2026–2034. This is a policy‑consistent scenario (not a sales forecast).

EU Electric Vehicle Trade Balance Evolution (2017-2023)

Key strategic findings (from Eurostat's 2017–2023 series):

- Import surge. EV/hybrid share of extra‑EU car imports jumped from 8% (2017) to 44% (2023). [32]

- China dominance. 49% of EU electric‑car imports in 2023 originated from China. [32]

- Export growth. EV/hybrid share of EU car exports rose from 2% to 27%. [32]

- Trade balance (context). Despite rising EV imports, the overall EU car trade surplus was €89.3 bn in 2024 (exports €165.2 bn; imports €75.9 bn). [33]

- Implication. The gap between fast‑rising EV imports and exports heightens the case for localised EV/battery production and power‑electronics talent in Europe; recent IEA trade/production data show strong competitive pressure from Chinese OEMs. [38]

- Strategic Implications: This trade dynamic creates urgency for localized EV production and talent development in battery technology and power electronics

Source: Eurostat, Growing EU trade of electric & hybrid cars, October 30, 2024; and Eurostat News, "EU car trade surplus: €89.3 billion in 2024," 1 Apr 2025. Official EU

Key Market Drivers

- Regulatory framework. The EU's CO₂ rules for cars and vans tighten through 2030 and require 0 g/km from 2035, which pushes OEMs toward zero‑emission models. AFIR sets binding charging‑network targets to support that shift. [34–35]

- Consumer adoption. Uptake improves as range and charging access rise and ownership costs fall: Europe surpassed 1 million public charging points in 2024 (>35% YoY growth), with the share of fast chargers continuing to rise; average lithium‑ion battery pack prices fell to $115/kWh in 2024. [36–37]

- Technological advances. Rapid progress in batteries (cost, chemistries) and in software/connected features. Cybersecurity (UNECE R155) and OTA update rules (R156) became mandatory for all new vehicles produced from July 2024, accelerating software‑defined vehicle capabilities. [39]

- Competitive landscape. Competition intensifies from new entrants, especially China‑linked OEMs: in 2024 ~60% of EU electric‑car imports came from China, and the share of Chinese OEMs in those imports rose to two‑thirds (vs 49% in 2023 [32]). [38]

Regional vs Global Automotive Talent Shortage Projection

Europe Skills Gaps

Global Tech Shortage

(TMT/Tech-wide)

2.3M (2025) → 4.3M (2030) projected shortage (Korn Ferry, TMT sector) — directional benchmark [28]

EU Tech Shortage

(TMT/Tech-wide)

620K (2025) → 1.2M (2030) projected EU shortage (estimated 27% of global TMT shortfall) — regional benchmark [28]

Europe's automotive base (~14.6M direct+indirect) faces simultaneous electrification and digitalization. The most acute gaps are in AI/data and battery roles (above), with software demand remaining structurally high across vehicle programs [1, 15, 16, 21, 26].

Ready to implement strategic talent planning?

→ View Automotive Deep Tech Hiring Priority MatrixEvidence-based framework for strategic talent acquisition 2025-2030

Talent Demand Forecast

Europe's automotive transition shifts workforce needs from mechanical to electrical systems, software, data/AI, batteries and cybersecurity. The Commission's 2025 Automotive Action Plan prioritises skills alongside innovation, confirming reskilling as a core competitiveness lever [40]. Eurofound's 2025 brief shows restructuring pressures heighten new skills demand over headcount [41–42].

Software Development

Software‑defined vehicles (SDV) drive sustained demand for embedded and safety‑critical engineers. Capgemini finds 92% of automotive organisations expect to operate as software companies [44]. Wards/Omdia shows SDV programmes scaling in Europe [45]. Perforce highlights code quality, safety and security as top concerns, reflecting regulatory complexity [46]. Stack Overflow's embedded surveys confirm high adoption of automotive development stacks [47–48].

Key skills: C/C++, AUTOSAR, ISO 26262 functional safety, real‑time OS, CI/CD for embedded [49–52].

Battery Technology

European Battery Alliance scales training across the battery value chain. EBA Academy aims to train 800,000 workers by 2025; 100,000 already trained by Dec 2024 [23, 25].

Key skills: electrochemistry, cell/pack design, thermal management, BMS hardware/firmware, recycling [23, 25].

Data Science & AI

EU AI Act (entered into force Aug 2024; phased application 2025–2026+) [8, 9]. Commission/JRC documents outline L3–L4 automated functions, driving perception and decision‑making talent demand [10, 11].

Key skills: machine learning, computer vision, sensor fusion, MLOps for edge/cloud [45, 55, 70].

Predictive maintenance typically reduces downtime by 30–50% and digital twin approaches have cut development times by up to 50% in reported cases [56] [53].

Cybersecurity

UNECE R155/R156 mandatory from July 2024 creates structural demand for embedded‑security and OTA specialists [39]. Combined with ISO 26262 functional safety, safety‑&‑security competence becomes hiring priority [49, 50].

Key skills: embedded security, threat modelling, vulnerability management, CSMS/SUMS design, OTA hardening [50–51].

Strategic Talent Framework: Build, Buy, Partner

Successfully navigating the automotive-deep tech talent transformation requires a comprehensive, multi-pronged approach. Leading organizations are implementing a unified "Build, Buy, Partner" framework that addresses both immediate needs and long-term capability development.

Integrated Talent Strategy Framework

BUILD

Internal Development & Reskilling

- Reskill mechanical engineers → electrical/software roles

- Cross-training programs for hybrid competencies

- Apprenticeship programs with technical colleges

- Internal mobility and rotation programs

BUY

External Hiring & Acquisitions

- Recruit from Big Tech (Google, Apple, Tesla)

- Poach talent from deep tech startups

- Acquire entire teams through M&A

- Global talent centers in tech hubs

PARTNER

Strategic Collaborations

- University research partnerships

- Joint ventures with tech companies

- Startup incubation programs

- Outsourced development teams

Strategic Integration: Leading automotive companies are implementing all three approaches simultaneously — scaling workforce reskilling programs, securing regulatory approvals for limited Level 3 deployments in select markets, and forming targeted collaborations with advanced robotics/AI partners. These moves align with the industry’s shift toward software-defined vehicles and policy frameworks now in effect [57] [10, 11] [39]. OEM & Policy Sources

Critical Roles & Hiring Strategies for 2025-2030

Based on industry research and interviews with automotive HR leaders across the EU

Software & AI Talent

- Full-Stack Automotive Software Engineers with AUTOSAR expertise

- AI/ML Engineers specialized in computer vision and sensor fusion

- Functional Safety Software Specialists (ISO 26262)

- Hiring Strategy: Establish software development centers in tech hubs; offer competitive compensation packages with equity components; implement continuous learning programs

Electrification Specialists

- Battery Systems Engineers with cell chemistry expertise

- Power Electronics Engineers for high-voltage systems

- Thermal Management Specialists for battery and power systems

- Hiring Strategy: Partner with battery technology startups; recruit from adjacent industries (consumer electronics, energy storage); develop university partnerships with specialized EV programs

Cybersecurity Experts

- Automotive Cybersecurity Architects (ISO/SAE 21434)

- Embedded Security Engineers for ECU protection

- OTA Update Security Specialists

- Hiring Strategy: Recruit from defense and critical infrastructure sectors; offer specialized training programs; implement security certification sponsorship programs

Cross-Functional Integrators

- Systems Engineers with both mechanical and software expertise

- Digital Transformation Managers

- Technology Roadmap Strategists

- Hiring Strategy: Develop internal talent through rotation programs; implement mentorship programs pairing traditional automotive experts with tech specialists; recruit from aerospace and defense industries